If you’re like most homeowners, your home insurance is one of the biggest expenses you face each year, with the average U.S. homeowner paying around $1,915 annually. But did you know there are simple ways to lower that cost without sacrificing coverage? Whether you’re searching for affordable home insurance options or looking to reduce your current rates, knowing how to lower your home insurance effectively can make a big difference in your budget. In this guide, we’ll cover practical strategies to help you find the best rates and discounts available.

What Affects Home Insurance Costs

Understanding what affects your home insurance rates is key to finding ways to lower them. Here are the main factors that influence your home insurance premiums:

- Home Features: The age, condition, and safety features of your home can affect insurance costs. Homes with updated electrical systems and security alarms typically have lower premiums.

- Coverage Amount: The more coverage you choose, the higher your premiums will be. Higher coverage limits generally result in higher rates.

- Deductibles: Choosing a higher deductible can reduce your premium, but you’ll need to pay more out-of-pocket if you make a claim.

- Insurance History: Your claims history and credit score can influence your rates. Frequent claims or poor credit often result in higher premiums.

- Location: Homes in disaster-prone or high-crime areas usually have higher premiums.

Step-by-Step Guide to Lowering Home Insurance Premiums

Lowering your home insurance premiums doesn’t have to be difficult. Here are some proven strategies:

Raising your deductible can significantly reduce your premium. Just be sure you can afford the higher deductible if you need to make a claim.

Installing security features like smoke detectors, burglar alarms, or a sprinkler system can lead to discounts. Insurance companies often reward homeowners who take steps to protect their property.

Don’t settle for the first quote you receive. Comparing quotes from different insurers can help you find the best rate. Many companies offer online tools for quick comparisons.

Combining home insurance with auto or other types of insurance can often result in discounts. Many insurers offer significant savings for bundling multiple policies.

Make sure your coverage matches your current needs. If you’ve made home improvements or added valuable items, updating your policy can help you avoid overpaying.

Discounts Commonly Offered by Insurance Providers

Insurance companies offer various discounts to help lower your home insurance costs. Here’s a list of common discounts you might be eligible for:

- Security System Discounts: If your home has a monitored security system, you may qualify for a discount. This includes burglar alarms, fire alarms, and even smoke detectors.

- Multi-Policy Discounts: Bundling home insurance with other policies, like auto insurance, often results in savings. Many insurers offer a discount for having multiple policies.

- Claims-Free Discounts: Insurers reward homeowners who have not filed claims for several years. If you’ve gone without making a claim, you might be eligible for a discount.

- Home Improvements: Upgrades such as new roofing, storm shutters, or updated electrical and plumbing systems can lead to discounts. Let your insurer know about any recent home improvements.

- Loyalty Discounts: Some companies offer discounts for staying with them over the years. If you’ve been with the same insurer for a long time, ask if you’re eligible for any loyalty discounts.

How to Compare Insurance Providers

When looking for the best home insurance, comparing different providers is important. Here’s how to evaluate them when comparing different providers:

- Coverage Options: Compare what each provider includes in its policies, including dwelling coverage, personal property coverage, liability coverage, and any additional features.

- Rates: Get quotes from multiple companies and compare similar coverage levels to find the most cost-effective option.

- Customer Service: Check reviews for each insurer. Look for feedback on customer service, claims handling, and overall satisfaction.

- Discounts and Savings: Compare the types of discounts offered. Some insurers may offer better rates or more discounts than others.

Choosing the Right Coverage Level

Selecting the appropriate coverage level for your home insurance is essential for balancing cost and protection. Here’s how to determine the right amount of coverage:

- Assess Your Home’s Value: Calculate the cost to rebuild your home in case of a total loss. This should include construction costs, materials, and labor.

- Evaluate Personal Property: Inventory your belongings and their value. Ensure your coverage limits reflect the value of your personal property.

- Consider Liability Coverage: Choose a liability limit that protects you from potential lawsuits or accidents on your property. Higher limits can provide more protection.

- Add Riders if Necessary: If you have valuable items like jewelry or art, consider adding riders to your policy for additional coverage.

Exploring State and Federal Programs for Home Insurance Savings

In addition to private insurance discounts, there are state and federal programs that can help reduce your home insurance costs. Here’s a look at some of these programs:

- State-Specific Programs: Some states, like Florida, offer programs to help homeowners in high-risk areas. Check your state’s insurance department website for options.

- Flood Insurance: The National Flood Insurance Program (NFIP) offers coverage for flood damage. This program is especially important if you live in a flood-prone area.

- Disaster Assistance: Federal assistance programs like those from the Federal Emergency Management Agency (FEMA) can provide support in the aftermath of natural disasters. While not directly reducing your insurance premium, these programs can help manage the financial impact of disaster-related damage.

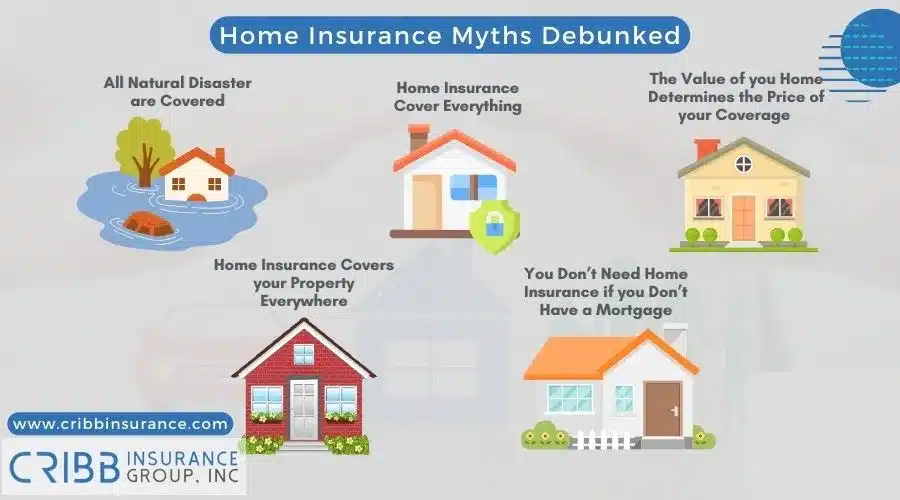

Debunking Common Myths About Home Insurance

There are several myths about home insurance that can lead to misunderstandings and potentially higher costs. Here are some common myths and the truth behind them:

- Myth 1: Home Insurance Covers Everything: Many believe home insurance covers all types of damage. In reality, standard policies may exclude certain types of damage, such as flooding or earthquakes. It’s important to review your policy and consider additional coverage if needed.

- Myth 2: Higher Premiums Mean Better Coverage: A higher premium doesn’t always guarantee better coverage. For example, some people think paying $3,000 annually guarantees top-tier coverage. However, paying less for the same coverage is often possible if you compare policies carefully.

- Myth 3: You Don’t Need Insurance if You Rent: Renters insurance differs from homeowners insurance, but it’s still important. It covers your personal belongings and liability, which are not included in the landlord’s insurance.

Guiding You Through Annual Insurance Policy Reviews

Regularly reviewing your insurance policy is crucial for ensuring you have the right coverage at the best price. Here’s how to conduct an annual review:

- Check Coverage Limits: Ensure your coverage limits are up-to-date with the current value of your home and belongings. Adjust limits if you’ve made significant home improvements or acquired valuable items.

- Compare Quotes: Each year, obtain new quotes from different insurance providers. Comparing these quotes can help you find better rates or discounts.

- Update Personal Information: Notify your insurer of any major changes, such as a home renovation, new security system, or changes in your living situation. These updates can impact your premium and coverage needs.

- Evaluate Deductibles: Review your deductible amount and assess whether it fits your budget. Sometimes increasing your deductible can lower your premium, but make sure you can afford the higher out-of-pocket cost if a claim is necessary.

Discussing the Impact of Home Renovations on Insurance

Home renovations can significantly impact your home insurance, both in terms of coverage needs and premiums. Here’s how renovations can affect your insurance:

- Increased Coverage Needs: Renovations, such as adding a new room or upgrading to high-end materials, increase the value of your home. You may need to adjust your coverage limits to ensure your new improvements are protected.

- Potential for Lower Premiums: Certain renovations can actually lower your insurance premium. For example, installing a modern security system or upgrading to impact-resistant roofing can qualify you for discounts. Check with your insurer to see if your renovations make you eligible for savings.

- Updated Policy Information: Inform your insurance company about any significant changes to your home. This ensures your policy reflects the current value and condition of your property and helps prevent issues with claims in case of damage.

Your Path to Affordable Home Insurance Starts Now

Lowering your home insurance premium involves smart strategies and careful planning. By taking advantage of discounts, exploring state and federal programs, and regularly reviewing your policy, you can reduce your insurance costs while maintaining adequate coverage. Home renovations and accurate information about your home’s value can also impact your premiums.

Stay informed, and review these steps regularly to manage your home insurance effectively and ensure you’re getting the best deal possible.

Frequently Asked Questions

How often should I review my home insurance policy?

Reviewing your home insurance policy annually or whenever you make significant changes to your home is a good idea.

Can I lower my premium if I improve my home’s security?

Yes, many insurers offer discounts for home security improvements, such as installing alarms or deadbolts.

Are there specific discounts available for first-time home buyers?

Some insurance companies offer discounts for first-time home buyers, but it varies by insurer. Ask about available discounts when shopping for a policy.

What should I do if I find a lower premium with a different insurer?

Contact your current insurer to see if they can match the lower rate. If not, consider switching to the new insurer for potential savings.

Does my credit score affect my home insurance rates?

Yes, in many states, insurers use credit scores to determine premiums. Maintaining a good credit score can help lower your rates.

Ready to Save on Your Home Insurance?

Don’t leave your home insurance savings to chance. Review your current policy, explore available discounts, and compare quotes from different providers. Cribb Insurance Group Inc can help you take control of your home insurance costs today and ensure you’re getting the best value for your money. Contact us now for a personalized quote!

Check out these links for more resources about this topic:

https://www.pinterest.com/pin/1075938167221357691

https://www.youtube.com/watch?v=-7AnYkpFd0g

")